Nearly nine million borrowers are now in default, a number that has surged by more than 3.5 million since repayment resumed, with 2.6 million defaulting in Q1 2026 alone. More than one in five borrowers with a payment due are seriously delinquent – the highest rate ever recorded. And the One Big Beautiful Bill Act (OBBBA) just eliminated Grad PLUS loans for new borrowers, creating a funding gap that will affect hundreds of thousands of graduate students starting July 2026.

And somewhere right now, a loan operations team is manually reviewing documents in a shared inbox, copying data between three systems, and wondering why their pull-through rate keeps dropping.

This isn’t a crisis of demand. It’s a crisis of execution.

The student lending industry is sitting on the biggest technology gap in financial services, and the lenders who close it first will dominate the next decade.

The Operational Problem No One Wants to Talk About

Here’s the uncomfortable truth: most student loan platforms are running on infrastructure designed for a different era.

We’ve helped develop hundreds of loan programs and have intimate technical and operational knowledge with the largest origination platforms across the U.S. (and internationally). The pattern is almost always the same:

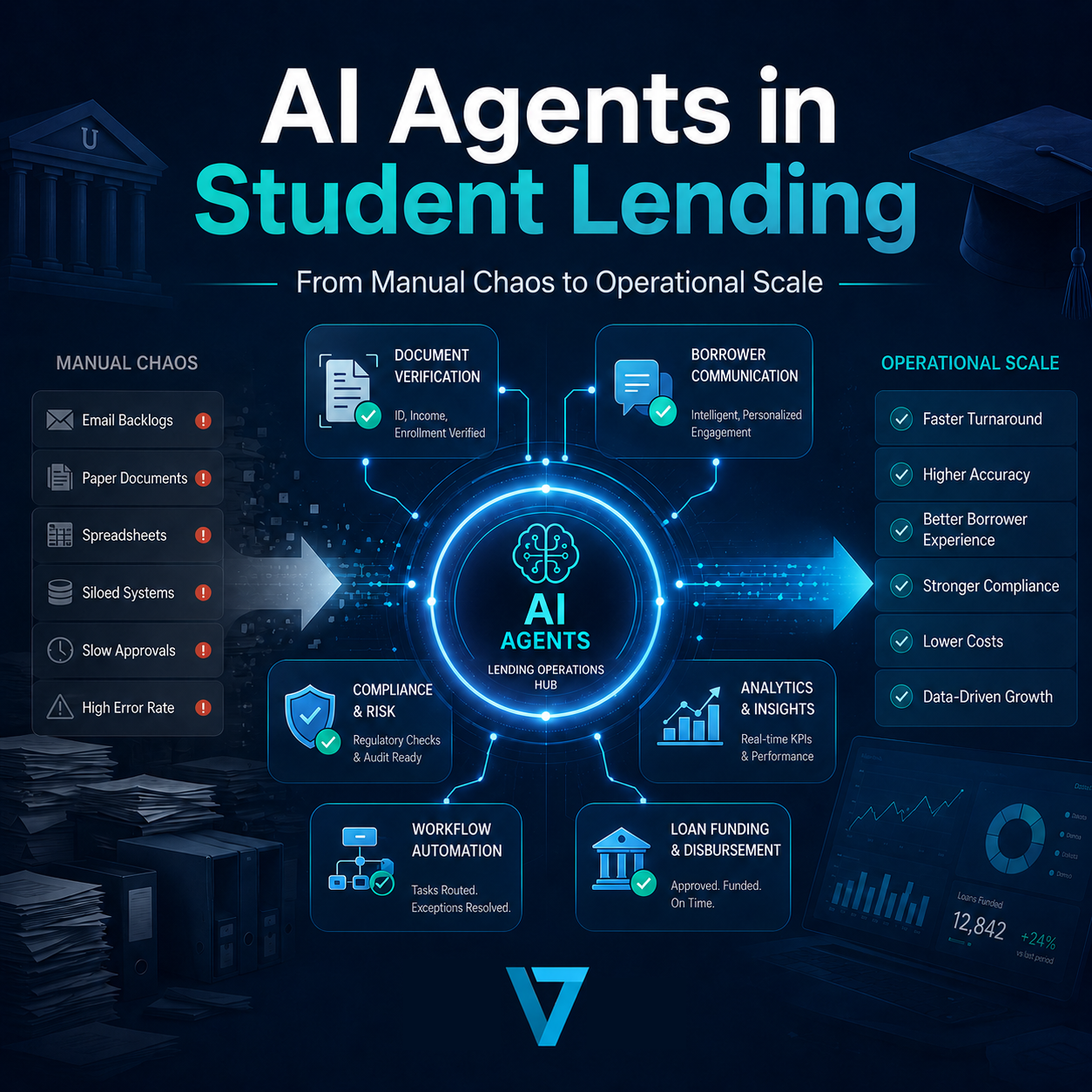

- Document verification takes days, not minutes. Borrowers upload income statements, school certifications, and ID documents… then wait while teams manually review, request re-uploads, and chase missing paperwork through slow, old school email chains.

- Status updates are invisible. Approved borrowers can sit in pipeline limbo for days/weeks, unsure if their loan is progressing. The result? They rate-shop, get poached, find another lender, and cancel. Pull-through rates collapse!

- Systems don’t talk to each other. CRM data sits in one system, the LOS in another, marketing analytics in a third. Teams spend more time reconciling data than acting on it.

- Seasonal scaling is a nightmare. Peak enrollment season hits, application volume triples, and suddenly you’re scrambling for temporary staff who take weeks to train on your workflows.

These aren’t edge cases. This is the operational reality for the majority of student lenders and nearly every major loan origination platform we’ve seen.

The cost? McKinsey estimates that banks using legacy manual processes spend 30% more on loan operations than those with modern automation. Deloitte puts the automation opportunity for non-core manual tasks at up to 40% of total workload. JPMorgan’s automation of commercial loan agreement review alone saved over 360,000 hours per year.

In student lending specifically, the math is brutal. Every day a borrower spends stuck in document verification is a day they lose confidence in the lender and might find a competing offer. Every manual touchpoint is a chance for human error, compliance risk, and borrower frustration.

Enter AI Agents: Not Chatbots. Operational Teammates.

Let’s be clear about what we mean by “AI agents”, because this is NOT about bolting a chatbot onto your FAQ page.

AI agents are autonomous digital workers that handle real operational tasks: document intake and verification, borrower communication, status updates, compliance logging, and exception routing. They don’t replace your team. They handle the 70% of repetitive work that’s crushing your team’s capacity to do what actually matters — close loans, build relationships, and solve problems.

Here’s what this looks like in practice:

Document Verification in Minutes, Not Days

An AI agent receives a borrower’s uploaded documents, extracts data using intelligent document processing, cross-references it against application data, flags discrepancies, and either auto-approves or routes exceptions to a human reviewer, all within minutes of submission. Current benchmarks show at least a 50% reduction in turnaround time for document processing with AI-powered systems.

For a lender processing thousands of applications during peak season, this isn’t incremental. It’s transformational.

Borrower Communication That Actually Moves the Needle

The #1 reason approved borrowers cancel? Silence. They don’t know what’s happening, they don’t feel supported, and a competitor remarketing ads will shows up at exactly the right moment.

AI agents solve this with personalized, behavior-triggered communication across email, SMS, chat and even outbound calls. A borrower who uploaded documents two days ago but hasn’t received a status update? The agent sends a proactive message. A borrower who was approved but hasn’t signed? The agent follows up with next steps and a direct link. A borrower who’s stuck on a form field? The agent offers real-time, non confrontational support.

This isn’t about replacing human counselors. It’s about making sure no borrower falls through the cracks at 2 AM on a Sunday or a banking holiday when applicants are home, finishing up their to-do lists. Incorporating 24/7 digital support can be the difference between a funded loan and an abandoned application.

Intelligent Pipeline Management

Instead of operations managers manually reviewing pipeline reports every morning, AI agents continuously monitor loan status, flag aging applications, identify bottlenecks, and surface the highest-priority actions for human review. Think of it as a really smart Work Queue that doesn’t need coffee breaks.

Applications sitting in doc verification for more than 24 hours? Flagged. A cohort of borrowers with an unusually high cancel rate? Surfaced with root-cause analysis. Pull-through trending 5% below your rolling average? Alert with recommended interventions.

The Numbers That Should Keep Every CEO Up at Night

The fintech industry generated approximately $650 billion in revenue in 2025, growing 21% year-over-year, materially outpacing the broader financial services industry’s 6% growth. Separately, the U.S. private student loan sector represents a meaningful education-finance opportunity with approximately $144.9 billion as of Q1 2025, or about 8% of total U.S. student loans outstanding. New OBBBA federal loan limits and the phaseout of Grad PLUS loans are expected to increase reliance on private borrowing. This includes roughly $8 billion of graduate loan volume above the new federal limits, creating a potential demand shock.

But here’s what’s really happening beneath the surface:

- AI-enabled fintechs are building products in weeks that legacy lenders take a year or more to develop. McKinsey’s 2026 fintech report calls this the single most consequential force reshaping the industry.

- The compliance landscape is fragmenting. With federal oversight retreating and states rushing to fill the regulatory void, operational complexity is increasing, not decreasing. Manual compliance management simply doesn’t scale.

- International student lending is exploding. From Africa (where innovative fintechs are using income-share and alternative credit models) to Latin America (50% annual lending growth since 2021), the global opportunity demands operational infrastructure that can cross borders, currencies, and regulatory frameworks.

- The OBBBA is creating a massive private lending opportunity — and the lenders who can originate, process, and fund loans fastest will capture the lion’s share of borrowers who can no longer rely on Grad PLUS.

The winners in this market won’t be the lenders with the lowest rates. They’ll be the lenders with the fastest, most frictionless, most reliable and celebrated borrower experience — from first click to funded loan.

What “Good” Actually Looks Like

We’ve spent two decades helping lenders go from concept to $1 billion+ in originations. Here’s what separates the programs that scale from the ones that stall:

1. Unified data architecture. Your CRM, LOS, analytics, and marketing platforms need to talk to each other in real-time. If your ops team is exporting CSVs and building pivot tables to understand pipeline health, you’re already behind.

2. AI-augmented operations (not AI-replaced teams). The best implementations are pairing AI agents with experienced loan counselors. The agent handles intake, verification, communication, and routing. The human handles judgment, relationship building, and complex exception resolution. This hybrid model consistently delivers the highest pull-through rates.

3. Real-time borrower intelligence. Every interaction a borrower has with your platform (every page visit, every document upload, every abandoned form) should feed a real-time profile that triggers the right action at the right time. This is where AI moves from “nice to have” to competitive weapon.

4. Compliance as code, not as checklist. Regulations change. AI agents can be updated to reflect new requirements across your entire operation in hours, not weeks. When you’re operating across multiple states (or countries), this is the only way to scale without multiplying headcount.

5. Speed to market. The OBBBA opportunity has a window. The lenders who deploy new products, partnerships, and borrower experiences in the next 12 months (while competitors are still in committee meetings), will establish the market positions that last a decade.

The Question Isn’t Whether to Automate. It’s How Fast You Can Move.

Here’s what we tell every lender we work with: the technology isn’t the hard part. AI agents, intelligent document processing, real-time analytics, automated compliance — these tools exist today. They’re proven. They’re affordable.

The hard part is the strategic clarity to know where to start, the operational expertise to implement without disrupting live portfolios, and the industry knowledge to avoid the wildly expensive mistakes that come from deploying fintech solutions without fully understanding this specific lending niche.

That’s the gap we fill at Valet. We don’t sell software. We build, launch, and scale lending programs, and we embed the technology, processes, and intelligence that turn good programs into market leaders.

Hundreds of programs. Over two decades. The playbook works.

If you’re running a student lending operation, whether you’re a startup with a single program, a national platform managing billions, or an international fintech serving markets traditional lenders won’t touch – and you know your operations should be smarter, faster, and more scalable than they are today, let’s have a conversation.

The lenders who automate will eat the lenders who don’t.

The question is which side of that equation you want to be on.